Content

Every individual company will usually need to modify the eight-step accounting cycle in certain ways in order to fit with their company’s business model and accounting procedures. Modifications for accrual accounting versus cash accounting are usually one major concern. The accounting cycle is used comprehensively through one full reporting period. Thus, staying organized throughout the process’s time frame can be a key element that helps to maintain overall efficiency. Most companies seek to analyze their performance on a monthly basis, though some may focus more heavily on quarterly or annual results. Now that you have recorded your transactions, the next step is to post them to the ledger.

What is step 6 of the accounting cycle?

Step 6: Closing the Books

In the accounting cycle steps, the last step is for a company to close its books at the end of the day on the closing date. The closing statements give a report that can be used to look at how well things went over the period.

Factors that should be considered when making decisions include the company’s financial position, Cash Flow, profitability, and business strategy. Accountants use the information to make decisions by analyzing data and trends to make informed decisions to help the company achieve its goals. The goal of preparing an unadjusted trial balance is simply to ensure that all debits and credit balances are equal. If you work for a business in the accounting department, you’ll quickly become familiar with the accounting cycle. At the end of the accounting period, you’ll prepare an unadjusted trial balance.

Reversing Entries

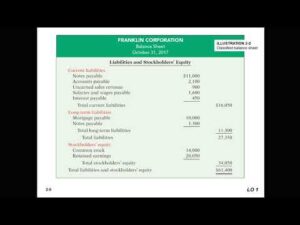

The unadjusted trial balance is the first trial balance that must be prepared. This balance is a listing of all the ledger accounts after all entries are posted. Usually, this listing is prepared at the end of a financial period.

Another example will be if a business receives $1,000 in cash for services rendered. The transaction analysis would involve identifying the accounts affected (cash and revenue) and determining https://marketresearchtelecast.com/financial-planning-for-startups-how-accounting-services-can-help-new-ventures/292538/ how it affects the accounting equation. In this case, the assets (cash) increase by $1,000, and the equity (revenue) also increases by $1,000, keeping the accounting equation in balance.

Translate the Adjusted Trial Balance to Financial Statements

The Balance Sheet accounts such as Assets, Liabilities and Equity need to be carried forward to the next period since they are ongoing parts of the business. Other columns include the date of the transaction, the accounts effected as well as the source material used for developing the transaction. The first step involves Bookkeepers bookkeeping for startups who document ALL daily transactions. Regardless of the number of transactions or the size of the organization, the steps involved are similar. The purpose of the Accounting Cycle is to convert ALL the transactions that have happened in the business into meaningful financial information for the reader through Financial Statements.

Once a transaction is recorded as a journal entry, it should post to an account in the general ledger. The general ledger provides a breakdown of all accounting activities by account. This allows a bookkeeper to monitor financial positions and statuses by account.

Step 2: Record Transactions in a Journal

Accountants follow the procedures outlined in Generally Accepted Accounting Principles. Mainstreaming the accounting process ensures that any accountant or auditor can track financial data back to its original transaction. The accounting process has nine or 10 steps, depending on your company’s preferences, that are completed at different times during an accounting cycle.